As 2023 wraps up, we discuss what has happened this year and what we expect in 2024 in this WJNotes. We also describe trades to be placed over the next month.

A lot of activity and little progress summarizes markets over the past few years. Balanced stock and bond portfolios are mostly flat and only a few broad-based indexes are at new highs. Why?

We blame inflation. Inflation peaked at 9.0% in June of last year at a level not seen since 1981. Fortunately, it has declined to 3.1%, although it remains above the FED’s (“Federal Reserve”) 2.0% target.

We also blame the FED and its aggressive efforts to fight inflation. Simplistically, the FED focuses on two goals. The first goal is to ensure people have jobs, while the second goal is to maintain low and stable inflation. The problem is these can be competing objectives. Low unemployment is associated with a strong economy which can cause high inflation and vice versa. So, to balance their goals, the FED has been increasing interest rates to bring down inflation, hopefully without causing a large rise in unemployment. Historically, the FED has failed at this balancing act. Inflation has come down, but the economy has fallen into a recession. Alas, so far at least, this time appears to be different.

The following shows US unemployment.

The chart shows only a minor increase in unemployment since the FED started increasing rates (red circle). Unemployment remains at historic low levels not seen since the 1960s. To be fair there are signs of a slowing economy, but there are just as many indications of economic strength. Regardless, a recession does not appear imminent.

So why has inflation declined without a significant slowdown or recession and higher unemployment?

- As it turns out, maybe inflation was transitory. Inflation was caused by COVID-related supply and demand distortions and the robust Government response to COVID. As those effects waned and things have returned to normal, prices have stabilized. Maybe the FED’s aggressive interest rate increases weren’t necessary, and prices would have stabilized without their actions.

- It could be that the pain from interest rate increases has yet to be felt fully and a recession is looming. Historically, a recession due to rate increases starts months after the FED stops increasing rates. Assuming they are now done with rate increases if history repeats, we wouldn’t expect to see a recession until later in 2024.

- Maybe rate increases don’t matter as much anymore because the largest and most important companies in the US, like Apple, Microsoft, and Amazon, don’t rely on debt financing to operate their business. They are insensitive to interest rates.

- Or it could be we already had a recession in 2022 when GDP declined for two consecutive quarters, corporate profits fell, and stocks crashed.

We obviously don’t know the answer, but since no one else does either, it has led to significant volatility in financial markets. The impact has not been consistent across markets:

- Cash yields have soared to levels not seen since 2005, making cash more attractive, at least for now, as discussed below.

- Bonds, especially long-term bonds, have been devastated. Long term treasury bonds were down 50% from their highs a couple of months ago, while a typical bond index made up of treasury and corporate bonds is 15% off its recent high. It has been painful for bond investors, but like most investments, the drop in value has led to substantially greater expected future returns as we discuss below.

- Stocks have treaded water, making no progress for several years, but it has not been a straight line. Stocks suffered significantly last year but strongly rebounded this year.

The net result has been flat performance for most balanced stock bond benchmarks over the last three years.

The bright spot for WJ portfolios has been alternatives:

- Last year, managed futures or trend following investments, appreciated 22% as they bet against bonds and increasing interest rates.

- This year, Reinsurance soared as the combination of rising premiums and no major disasters led to a 43% increase.

What does this mean for the future?

Bond returns should be far superior to the last 15 years. Since the financial crisis in 2008, bonds have returned about 1% per year. Today bond yields are about 5%. Since the current yield is a reasonable predictor of future returns, we expect bond returns of around 5% for the next 5 to 10 years. And if interest rates fall, bonds will capture some of this future yield immediately which we discuss in more detail below.

Stocks outside the US look inexpensive and even US stocks, outside of the magnificent seven (the largest tech-oriented companies like Google, Microsoft, Apple, etc.), appear attractively valued, which could mean higher returns in the future.

The net result is forward returns for our balanced stock and bond benchmarks appear better than we’ve seen in years.

One cautionary note we would add. We’ve heard from some clients that high cash yields make investing in bonds and stocks unnecessary. We don’t agree. It is time to invest your cash.

Today, you can earn 5% on your cash if you put it in Flourish Cash or something similar at a high-yielding bank. However, this yield is subject to change, and in fact, the market is predicting about 1.25-1.5% in interest rate cuts over the next year. That means you’ll earn something closer to 4-4.5% over the next year, depending on the timing of those cuts. And since cash is taxed as ordinary income, you could lose 30% or so to taxes (depending on your particular ordinary income tax bracket) each year leaving you with an after-tax return of around 3%.

With bonds, you also pay ordinary income tax on the interest, however, any price appreciation (which we’ll expand on in a moment) is taxed at the capital gains rate of 15-20%. In addition, municipal bonds, which are not taxable, yield about 4% today and have the potential for price appreciation. With stocks, most of the return is taxed at the capital gains rate of 15-20% and can be deferred.

Tax situation aside, we’ve been urging clients to invest cash simply because stocks and especially bonds look more attractive on an investment basis as mentioned above.

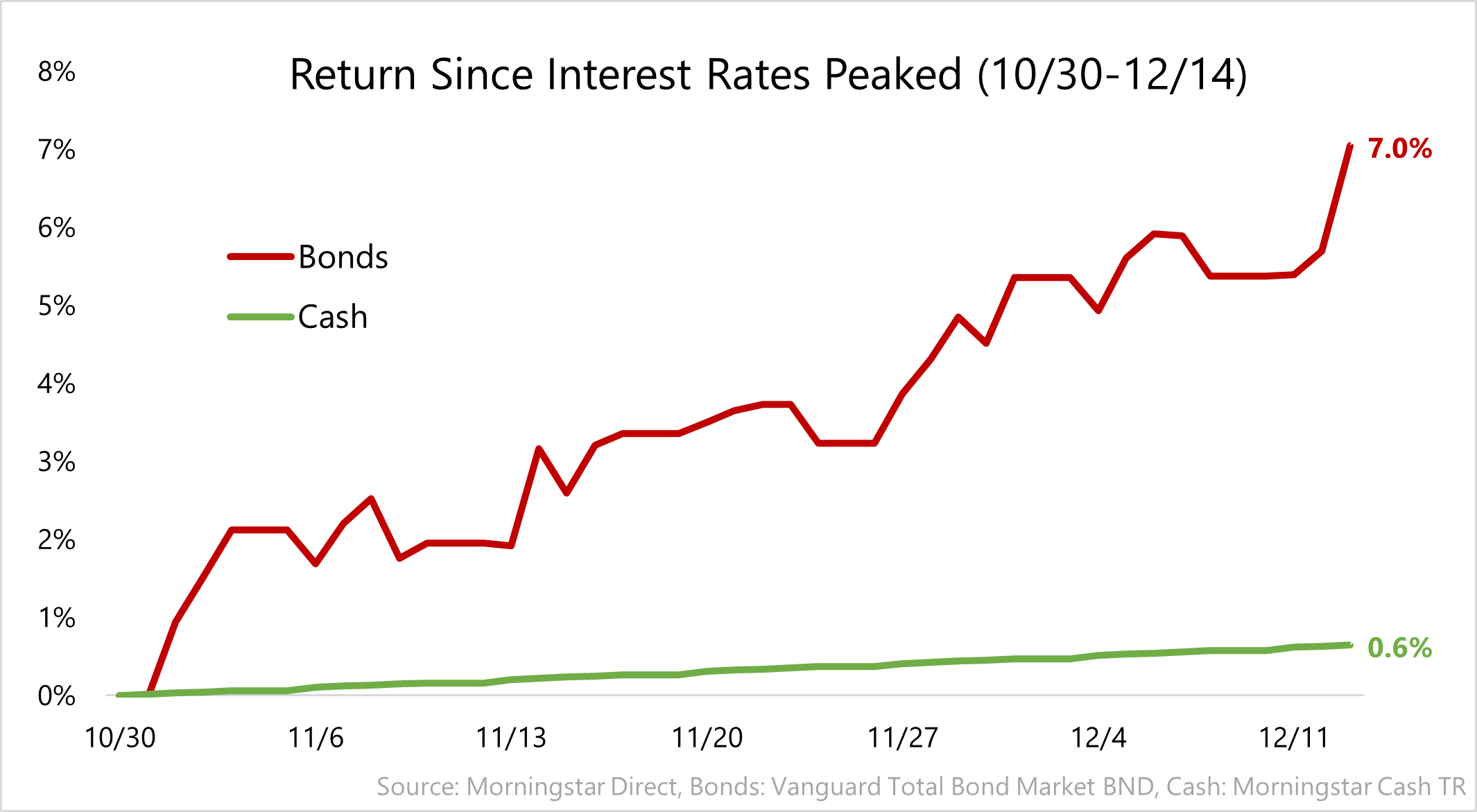

With bonds, the appeal is more obvious. For starters, our bond portfolio has a higher yield than cash (~6% vs 5%), but perhaps more important is the potential for price appreciation beyond just the yield. The FED is done raising rates, which likely means we’ve seen peak interest rates. Assuming bond yields fall, bonds will increase in price AND earn the yield. The rough math for our bond portfolio is it will appreciate about 7% per 1% drop in yields.

We’ve already seen this since the start of November, as the chart shows, but we believe yields can fall further.

Based on this outlook we are making some changes to portfolios through the end of this year and into the beginning of January.

First, we’ve discussed in the past how we utilize levered investments like exchange traded funds (“ETFs”) to get efficient exposure to stocks and bonds. This frees up cash to purchase diversifying alternatives like managed futures and reinsurance.

In that same vein, we are adding a new fund called Return Stacked® Global Stocks & Bonds (RSSB), which buys $1 of global stocks and $1 of treasury bonds for every $1 invested in the fund (2x Exposure). As said earlier, future stock and bond returns look more attractive than they have historically, and this fund gives us more of each without us having to sell alternatives.

In addition, we are changing our exposure to interest rates within the bond portion of the portfolio. We are buying Simplify Short-Term Treasury Futures Strategy ETF (TUA), which gives us enhanced exposure to 2-year treasury futures. Longer-term bond yields have already started to fall aggressively and may be nearing a normal level. Shorter-term yields, however, remain elevated, and we expect these to fall by a larger amount. TUA allows us to isolate the shorter portion of the bond curve and benefit if shorter rates fall.

We are selling the AQR International Defensive Style Fund (ANDIX) and putting those proceeds into the AQR International Multi-Style Fund (QICLX), which we already own. This is a simple way to consolidate positions, while also slightly increasing the beta (stock risk) of the stock portfolio.

Finally, we currently own the GMO Benchmark-Free Allocation Fund (WABIX) through a mutual fund company called Allspring. They have decided to change the underlying strategy, so we have been given access to the original GMO Mutual fund (GBMIX) in its place. We will do a simple swap of the two mutual funds, but the underlying strategy will be the same.

Please contact us if you would like to discuss these portfolio changes and how they impact your portfolio.

Thank you for your ongoing support of WJ Interests. We truly appreciate the trust you place in us. We hope everyone has a Merry Christmas and a Happy New Year.

DISCLOSURE: PAST PERFORMANCE IS NOT A GUARANTEE OF CURRENT OR FUTURE RESULTS. Historical examples included in this WJNotes do not, nor are they intended to, constitute a promise of similar future results. The WJ benchmarks represented herein are the benchmark allocations from which most client portfolios are designed. Specific client portfolio allocations, risks and returns can and may deviate from these benchmarks depending on accounts and types of investments available through each account. Future market views by WJ Interests, LLC may vary significantly from the historical examples presented herein and no one receiving this summary should assume that WJ Interests, LLC will be able to replicate successful views in the future.

Benchmarks mentioned are as follows:

| US Large Stock | iShares Russell 1000 (IWB) | |||||||||||

| US Small Stock | iShares Russell 2000 (IWM) | |||||||||||

| Intl Developed Stock | iShares Core MSCI EAFE (IEFA) | |||||||||||

| Intl Emerging Stock | iShares Core MSCI Emerging Markets (IEMG) | |||||||||||

| Bonds | Vanguard Total Bond Market (BND) | |||||||||||

| Cash | Morningstar USD 1M Cash TR USD | |||||||||||

| Reinsurance | Stone Ridge Reinsurance Fund (SRRIX) | |||||||||||

| Managed Futures | SG Trend Index, PIMCO Trends (PQTIX), Virtus Alphasimplex (ASFYX) | |||||||||||

| TAA | Allspring Absolute Return (WABIX) and Strategy Shares Nwfnd/Rslv Rbt ETF (ROMO) | |||||||||||